Some Good News for a Change: Better Libel Insurance Now Available for Smaller Newsrooms

Crafted with support from a leading philanthropy

Welcome to Second Rough Draft, a newsletter about journalism in our time, how it (often its business) is evolving, and the challenges it faces. This week’s edition is being published early to avoid the holiday.

Late last year, I wrote about what I described as an epidemic of inadequate libel insurance coverage of smaller newsrooms—a particular concern in light of the hostility to journalism being whipped up in many places by Trump and his acolytes, especially at the local level. This week, I am delighted to report that, after an exploration funded by a leading philanthropy (on which I served as a consultant), there is a solution.

The problem

My concerns were these: First, that many smaller newsrooms lacked media liability coverage altogether. Second, deductibles (a colloquial term similar to what is called “retention” in the insurance business) were sometimes so high that newsrooms were self-censoring important stories. Next, in the specialized field of libel law, where nearly every case presents issues of complex constitutional law, many policies did not adequately guarantee qualified defense counsel. Coverage limits were sometimes too low, considering the current climate and cost of defense. And finally, some policies enabled insurance carriers to settle cases for economic reasons even when challenged stories were accurate and entirely legally defensible (in the insurance business, such policies are said to have a “hammer” clause, sometimes a “soft hammer.”) The policy the philanthropy’s efforts has produced avoids all of these problems.

The solution

The policy is being offered by Axis, a leading insurer with an “A” rating from AM Best and an “A+” from Standard & Poors, which has offered coverage in this space for more than 45 years. Neither the philanthropy nor I will receive any economic benefit from the sale of these policies; I also was not paid for the time it took to write or edit this column. Nor is the philanthropy subsidizing the coverage—this is a market solution, crafted with invaluable help from EPIC, a leading insurance broker, which is also not being compensated for its role here by the philanthropy.

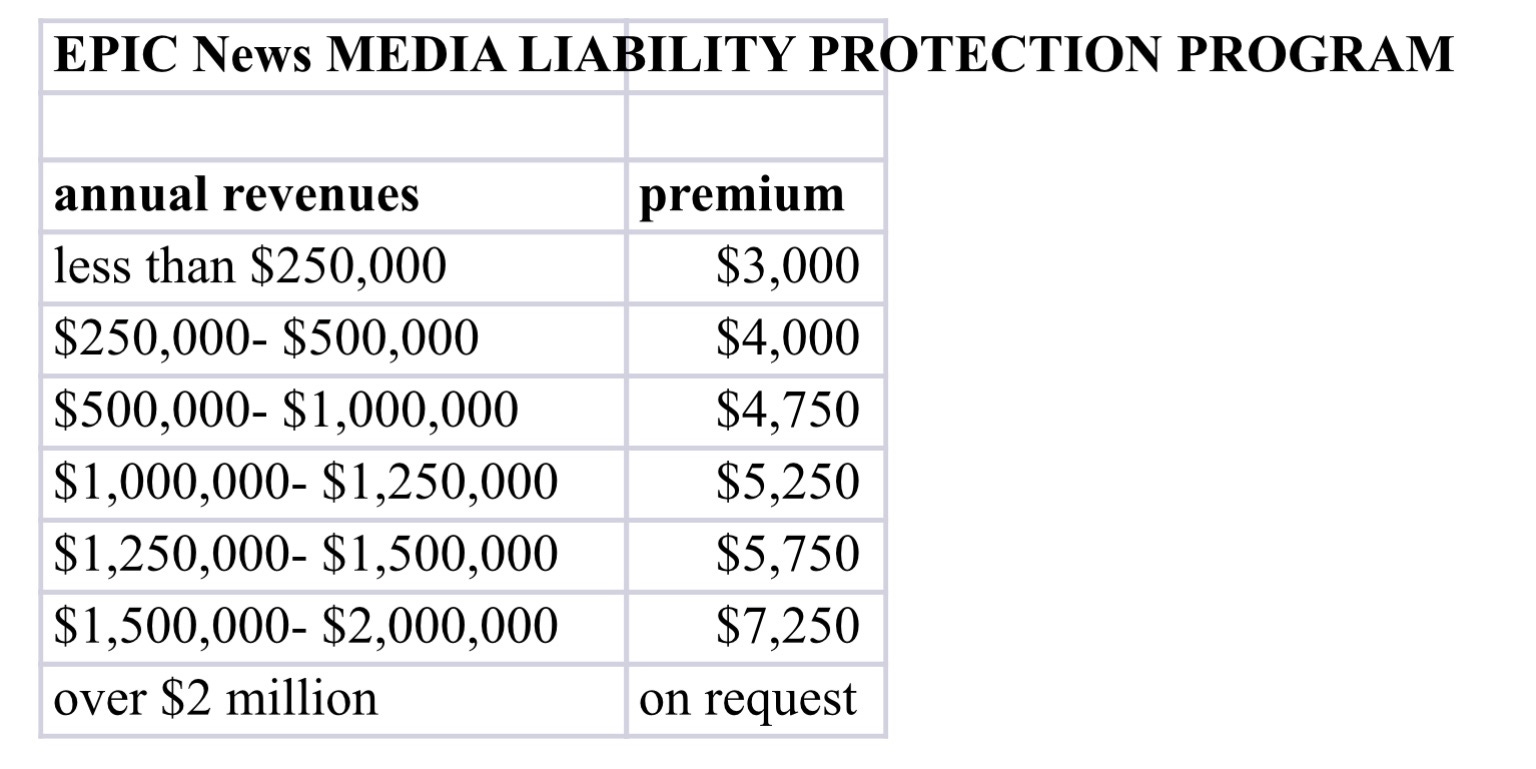

For newsrooms with annual budgets under $2 million, the retention will be an affordable $2500. In this climate, I recommend at least $2 million in coverage, and will refer below to premium costs at that level, although $1 million coverage limits are also available at slightly reduced cost. The Axis policy, with stronger pro-publisher language than that currently offered through one intermediary, contains no hammer clause, “soft” or otherwise, and five leading firms have been pre-approved as counsel, including what I regard as the three leading press defense firms in the country.

The cost of this coverage is about $3000 annually for the smallest newsrooms (under $250,000 in annual revenue), rising to a bit more than $7000 for those between $1.5-2 million. That seems to me both prudent as an expenditure and a modest burden. Taxes add slightly to the cost in five smaller states, and rates will also be higher for newsrooms principally involved in investigative reporting, which is, of course, riskier. Rates will also be higher, but coverage will still be available, for newsrooms with revenues over $2 million.

As with most such coverage, legal fees and other costs of defense do not count against the liability limits of the policy. And while I have described this as “libel” coverage, as most of us do, it is actually broad-based publisher’s liability coverage, including claims for invasion of privacy, slander, copyright infringement and subpoena defense. Cyber liability insurance is available at additional cost.

A point of contact, and other support

Brian Finnell of EPIC has been designated to handle questions, and provide help to newsroom applicants. He’s reachable at EPICNews@epicbrokers.com and (631) 390-9710.

In anticipation of the launch of this new insurance I reached out to a number of people in our industry, including the leadership of the Institute for Nonprofit News and of LION Publishers, which were both very supportive.

“In our deep evaluative work with more than 350 independent publishers, we found more than half of them – 53 percent – do not carry media liability insurance, which puts everything they’ve built at risk,” said Chris Krewson, executive director of LION. “The plan LION helped shape and launch a few years ago was a first step, but we’re very excited to see this new entry in the market build upon that foundation. We encourage every member of LION, and every independent publisher in the U.S., to carry media liability insurance and protect their businesses.”

"We're appreciative of this insurance option for independent news organizations and we, at INN, believe it will be both useful to and affordable for our smaller member newsrooms," said Karen Rundlet, executive director and CEO of INN.

I am really pleased we have been able to make this progress on an important element of support and risk mitigation, especially for smaller newsrooms. I would especially appreciate your sharing this edition of Second Rough Draft with any editor, publisher or group of newsroom leaders you think might benefit from this new offering.

So great to hear. I’m very curious if they’d be open to an even lower tier for independent journalists

Excellent idea, very much needed. Thanks for working on it.